This research post begins with two simple premises in mind: (1) Sometimes financial advisors charge their customers excessive commissions or advisory fees; (2) When this does occur, the customer—who likely has reposed great trust in his or her financial advisor—has no idea that excessive commissions or fees were charged. After all, it stands to reason that if customer was aware they were being overcharged, they would have objected.

The practice of charging excessive commissions is often referred to as “churning.” Unsophisticated, retired, elderly investors are particularly vulnerable to churning brokers.

Here, we briefly examine six (6) ways an unscrupulous broker or financial advisor charges excessive fees or commissions in the accounts of unsuspecting customers.

It is a longstanding principle in the securities industry that the fees and commissions brokers and financial advisors charge their clients must be fair and appropriate. In 2003, for instance, the NASD (FINRA’s predecessor entity) issued Notice to Members 03-68 to brokerage firms, reiterating a statement it made in 1975 emphasizing that “charges must be ‘fair under the relevant circumstances and a member should be prepared to justify that its prices are fair as to each customer and transaction.’” Nonetheless, churning remains a leading source of new arbitration cases filed in the FINRA arena.

Churning brokers and financial advisors have many techniques at their disposal to extract excessive fees and commissions from their clients. Attorney Montgomery G. Griffin spent nearly a decade working as a financial advisor at two major Wall Street firms, giving him special insight into how brokers and financial advisors generate (and sometimes even conceal) excessive fees and commissions. They include:

- Initial Public Offerings/Syndicate Purchases. Initial Public Offerings (or “IPOs,” or “new issues” or “syndicate purchases” as they are known on Wall Street) are sold pursuant to an offering statement or prospectus. Brokers and financial advisors often pitch IPOs to clients as though they are “commission free” and that they are doing the clients a favor by getting them in early on an investment. However, the reality is that much of the time the broker or financial advisor is heavily incentivized to sell the IPO. Many IPOs have “selling concessions,” which are large commissions (often around 3% of the total purchase price) paid to the broker or financial advisor for selling the IPO to a client. These selling concessions—which routinely appear on the broker’s internal “commission runs”—are hidden within the lengthy and complicated prospectuses that accompany the investments, which investors invariably never read (or usually do not understand even if they try to read them). Furthermore, because the commission is obtained indirectly through a deal with the issuing firm (rather than straight from the investor), brokers and financial advisors (and their so-called “expert witnesses”) may attempt to misrepresent to arbitration panels that selling concessions are not commissions to investors and thus have no impact on the results in an account. When explained to arbitrators by an experienced advocate, it becomes evident that Wall Street’s position on selling concessions is disingenuous and designed to mislead. Cases relating to IPO transactions are often filled with nuanced arguments, only further exacerbating the need for an investor to have an advocate who is sophisticated and experienced in the world of securities and IPO transactions. The Law Offices of Montgomery G. Griffin have pursued multiple selling-concession-related cases with substantial success.

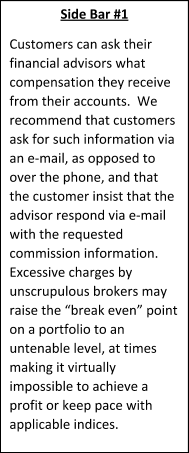

- Excessive Advisory Fees (or “Wrap Fees”). It is increasingly common for brokers and financial advisors to compensate themselves in the form of a fee, the amount of which is based on the total account value being managed by the financial advisor. These fees are commonly referred to as “advisory” or “wrap” fees. An advisory or wrap fee is charged in lieu of charging commissions in the account on a per-transaction basis. The percentage amount of the fee relative to the account’s value will vary depending on the assets under management, but fees generally are within the range of 0.10% to 2.00% annually. The average annualized advisory fee on one million dollars under management by the advisor is approximately 1.00%. If the client has less than a million dollars under management, the fee might be higher than 1% per year, and if the client has more than a million dollars under management, it is expectable that the fee will be lower than 1% per year. Advisory fees in excess of these guidelines are generally a red flag worthy of further investigation.

- Reverse Churning. Advisory fees should not only be reasonable in amount (as discussed above), they should also be appropriate for the accounts to which they are applied based on the level of activity in the accounts. In the words of the NASD in Notice to members 03-68, “fee-based programs are particularly appropriate for . . . those that engage in at least a moderate level of trading activity.” If there is a relatively low level of activity in a client’s account, such as when a long-term buy-and-hold strategy is being employed (often the case with bond-based or fixed income accounts), a client is likely better off paying commissions on a per-transaction basis. The practice of charging a client an unnecessary advisory fee (due to a relatively low level of activity in the account) is referred to as “reverse churning.” With a rise in popularity in recent years of advisory fees, reverse churning has become an increasingly pervasive problem and has received rapidly increasing attention from regulators.

If your broker or advisor is charging advisory fees on an account while engaging in relatively little “buy” and “sale” activity in the account, you may be a victim of reverse churning fraud.

One “red flag” indicative of reverse churning is where the broker or financial advisor enters relatively small and (in reality) essentially meaningless transactions in a customer’s account in order to try to create the impression that the account’s level of trading activity justifies charging an advisory fee. For example, we have seen examples where a so-called “financial advisor” entered a flurry of transactions, each involving less than $1,000 in value, in a million dollar account—an obvious attempt to create the (false) impression that the account had appropriately been placed in an advisory-fee platform.

4. Churning. It is hard to conceive of a more deceitful investment practice than churning. In the words of the SEC, “churning occurs when a broker engages in excessive buying and selling of securities in a customer’s account chiefly to generate commissions that benefit the broker.” One famous federal district court judge classified churning as being worse than ordinary theft since, unlike theft, the victim has no idea they are being fleeced when a broker churns an account.

When an account is charged commissions on a per-transaction basis (as opposed to a set advisory fee), an unscrupulous broker may engage in frequent buying and selling to generate substantial commission charges. Brokers engaged in such fraud frequently coax their clients into believing that this activity is in the client’s best interests, that it is some kind of “active” strategy designed to maximize gains or actively fend off losses, but in reality, the only gains being maximized are those of the broker and the firm.

It can also be extremely difficult for a retail investor to determine when an account is being churned. Aside from the fact that most retail customers struggle to understand when transaction activity in their account has become too much, trade commissions on individual transactions are frequently disclosed only on trade confirmations (but not on monthly account statements). To make matters worse, in recent years, brokerage firms have encouraged clients to receive their trade confirmations electronically, which helps a churning broker avoid the often-asked question “why I am receiving all of these trade slips in my mailbox at home?” from the victimized customer. Also, in the case of principal transactions, where the security is purchased by the customer directly from the brokerage firm’s own inventory, the commission may be disclosed only in the form of a confusing “markup” that requires rather sophisticated calculations to reveal the total commission charge in dollars.

Also, in some cases, the total transaction commission may not be discernable from the trade confirmation at all, such as when the security purchased is a mutual fund with an up-front “sales load” that is disclosed in a lengthy prospectus that investors invariably either do not know about or do not read.

Certain hidden commissions—like those often taken on municipal bond transactions or open-end mutual fund purchases—can be so large that churning can be achieved with only a few transactions in such securities.

Churning brokers have many crafty ways of obscuring the commissions they are generating. To determine whether churning has occurred, a complex and comprehensive expert forensic analysis must be conducted in the accounts and evaluated by an attorney knowledgeable about securities-related laws and standards. The securities fraud Law Offices of Montgomery G. Griffin has extensive experience analyzing, prosecuting, and winning churning cases.

5. Hybrid Schemes. A hybrid scheme is a combination of (3) and (4) above. In a hybrid scheme, the financial advisor talks the customer into opening both a commission account and a (wrap fee) advisory-fee account telling the customer that this arrangement will permit the customer to participate in a wider range of opportunities than would otherwise be available to the customer. The financial advisor may then begin engaging in abusive behavior, such as by purchasing a security in the commission account (on which he charges a commission) then moving (or journaling) the security to the managed account so that he can then earn an ongoing advisory fee on the value of the position while it is held. That same advisor also might eventually transfer the security back to the commission account to sell it so that the unknowing investor is forced to pay commission on the sale, as well.

6. Private Placements. Commission abuses are also frequently found in private placements. Private placements are securities sold privately to select investors, typically relatively wealthy “accredited” investors. An investment where the client is asked to sign (an often very lengthy and complex) agreement, or fill out a questionnaire for the investment, is likely to be a private placement.

Investments being sold through private placements frequently pay large commissions—sometimes near 10% of the client’s total investment—to the brokers and financial advisors who recommend them to customers. Furthermore, investments sold as private placements carry a special risk of fraud and abusive structure. For example, Ponzi schemes are often conducted through private placements. Non-public investments are rife with potential dangers and are extremely difficult to evaluate—investors would be wise to beware when their brokers or financial advisors present them with a non-public “opportunity” in a security that is not publicly-traded on a major exchange.

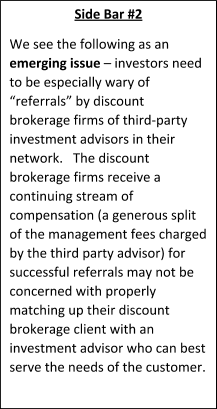

The above are just some of the ways that enterprising brokers and financial advisors might extract unwarranted commissions and fees from their clients. It is also important to note that commissions and fees are just one aspect of the costs that a client might incur in his or her accounts. Other costs, such as mutual fund expense ratios and options bid-ask spreads, may also adversely impact a client’s account performance. The Law Offices of Montgomery G. Griffin, in combination with forensic analysis experts with whom our firm consults, can assist you in determining whether your accounts have been charged fairly or whether you might have a basis for seeking legal recovery from your broker or financial advisor for excessive commission or cost abuses.